In 2024, Nigeria’s fintech sector dominated the tech investment landscape, securing 35% of total tech funding, which equaled $2 billion. This marked a slight decline from the 42% share seen between 2019 and 2023 but showcased the sector’s continued leadership. Fintech also accounted for an impressive 72% of equity investments in Nigeria, highlighting its strong investor appeal.

Key points:

- $2 billion raised by fintech startups in 2024.

- Nigeria became Africa’s top venture capital destination, attracting $520 million in equity funding, an 11% increase from 2023.

- Fintech was the only African tech sector to grow in both deal count (+16%) and total funding (+59%) despite a broader funding decline across the continent.

- Moniepoint‘s $110 million Series C round in October 2024 exemplified fintech’s dominance.

Other sectors like healthtech, e-commerce, logistics, and cleantech lagged behind in funding but showed potential for growth. For instance, healthtech startups expanded regionally, while e-commerce and logistics benefited from fintech infrastructure.

Fintech’s success stems from 83% mobile banking adoption, 76% profitability among startups, and a growing market of unbanked Nigerians. However, challenges like strict regulations and market saturation pose risks. Diversifying investments into other sectors could balance this volatility, although fintech remains the backbone of Nigeria’s tech ecosystem.

1. Fintech

Investment Volume

Nigeria’s fintech sector made waves in 2024, pulling in over $2 billion in investments. In just the first half of the year, Nigerian fintech companies secured $140 million across 24 deals – outpacing Kenya ($97 million), Egypt ($35 million), and South Africa ($34 million). This achievement stands out even more considering that total African fintech funding dropped by 77% compared to the previous year.

Some standout deals spotlight fintech’s resilience. In February 2025, Raenest secured $11 million in Series A funding, led by QED Investors, to enhance financial services for remote workers and freelancers. Meanwhile, PiggyVest reported paying out ₦835 billion (about $547.3 million) to users in 2024, a 53% increase from the previous year. These milestones helped fintech dominate the tech investment landscape, capturing 35% of total funding in Nigeria.

Share of Total Tech Funding

In 2024, fintech accounted for 35% of Nigeria’s total tech investments, a slight dip from its 42% share between 2019 and 2023. However, when it comes to equity funding, fintech dominated with a 72% share of Nigeria’s total equity investments. Across Africa, fintech attracted 60% of total equity funding, translating to $1.3 billion.

Stage Focus

Investor behavior in 2024 revealed shifting priorities. Seed-stage investments saw a 26% increase in ticket sizes, while Series A and B funding declined by 18% and 27%, respectively. Growth-stage funding was the only category to rise, fueled by large-scale deals. This trend underscores the sector’s promising revenue outlook and its ability to attract big-ticket investments.

Revenue Potential

Nigerian fintech companies are setting themselves apart with impressive revenue performance. A notable 85% of these firms are post-revenue, and 76% are already turning a profit. Even more striking, 57% of fintech startups report annual revenues exceeding $5 million. This financial strength is supported by strong market fundamentals – Nigeria ties with Turkey as the global leader in mobile banking activity, with 83% of adults using mobile banking services. Yet, half of Nigeria’s population remains unbanked, signaling significant growth opportunities.

“Africa’s financial services market could grow at about 10 percent per annum, reaching around $230 billion in revenues by 2025. Nigeria’s fintech sector makes up about one third of Africa’s fintech market.”

2. Healthtech

Investment Volume

In 2024, healthtech secured its spot as the third-largest sector by startup count. A standout example came in December 2024 when PBR Life Sciences raised $1 million in pre-seed funding. Backed by Launch Africa, XA Africa, and ARM Labs, the company aims to enhance its AI infrastructure while expanding operations into Ghana and Kenya. This focused regional growth highlights the rising interest and potential in healthtech.

Stage Focus

Investment trends in healthtech mirrored broader market shifts, with a noticeable preference for Seed+ funding rounds as Series A and B activity slowed. Investors have become more cautious, demanding solid metrics and compelling growth narratives before committing funds. This reflects the sector’s early stage and the need for startups to demonstrate sustainable business models before attracting significant capital.

Revenue Potential

Healthtech is deeply intertwined with Nigeria’s ICT sector, which contributed 18.9% to the country’s GDP in 2024 and is projected to reach 22% by 2025. With a young, tech-savvy population and increasing digital adoption, the sector is well-positioned for growth. Nigerian healthtech startups are also looking beyond borders, targeting markets like Ghana and Kenya for expansion. Additionally, advancements in AI and data analytics are fueling innovation, making healthtech a promising area for future venture capital investment. These developments set the stage for comparisons with other thriving sectors like e-commerce.

3. E-commerce

Investment Volume

E-commerce and Retail-Tech represent Nigeria’s second-largest tech subsector, with 58 startups compared to fintech’s 173. While fintech pulled in over $2 billion in 2024, e-commerce investments largely focused on seed and pre-seed rounds. The sector’s growth is increasingly tied to logistics infrastructure, with delivery-tech companies gaining significant attention from investors looking to enhance retail distribution.

In April 2024, Chowdeck, a food delivery and logistics-tech startup, secured $2.5 million in seed funding. The round included investments from YCombinator, Goldwater Capital, and the co-founders of Paystack, aimed at streamlining operations and expanding into more Nigerian cities. Just a month later, Renda, a logistics-tech company specializing in end-to-end fulfillment and retail distribution, raised $1.9 million in pre-seed funding. This included $1.3 million in equity led by Ingressive Capital and $600,000 in debt from Factory Africa and SeedFi. These funding rounds highlight how investment priorities vary across sectors.

Share of Total Tech Funding

Although fintech dominates overall funding, e-commerce and Retail-Tech play an important role by attracting niche investments focused on early-stage growth. Together, these startups make up 12% of Nigeria’s total startup ecosystem, a smaller share compared to fintech’s 36%. Between 2019 and 2023, fintech claimed 42% of cumulative tech funding, leaving e-commerce with a much smaller, unspecified share. The disparity underscores the challenges e-commerce faces in reaching the level of maturity and profitability that fintech has achieved.

Revenue Potential

Digital financial services such as mobile banking and digital lending are key drivers of e-commerce growth heading into 2025. With 187 million mobile connections (90% penetration) and a population where over 65% are under the age of 35, the conditions are ripe for online retail. In 2024, the telecommunications and ICT sector – which includes e-commerce – accounted for 18.9% of Nigeria’s GDP and is projected to rise to 22% by 2025.

“Nigeria’s fintech ecosystem… will continue to flourish in 2025, as digital financial services such as mobile banking, digital lending, and e-commerce expand.” – Office of the Special Adviser to the President on Economic Affairs

4. Logistics and Mobility

Investment Volume

Nigeria’s logistics and mobility sector is riding the wave of e-commerce growth, tapping into digital finance to attract substantial investments. While the sector comprises only 28 startups – a stark contrast to fintech’s 173 and e-commerce’s 58 – it has managed to secure some of the largest funding rounds in the country during 2024.

One standout example is Moove, a mobility startup specializing in vehicle financing for ride-hailing and logistics drivers. In the first half of 2024, Moove raised over $100 million in a single funding round, marking the only “mega-round” (deals exceeding $100 million) in Nigeria during that period. To put this into perspective, Nigerian fintechs collectively raised $140 million across 24 deals in the same timeframe. Moove’s funding round included a significant contribution from Uber, underscoring the growing appeal of the “fintech-plus-mobility” business model.

“After years of multiple fintech mega-rounds in H1, only Nigeria’s Moove raised over $100M in H1 2024.” – Chinwe Michael, Financial Journalist, BusinessDay

This massive deal highlights the sector’s ability to attract high-value investments, setting it apart from the smaller, more frequent seed rounds dominating other industries.

Stage Focus

Unlike fintech, where seed and pre-seed rounds are common, investments in logistics and mobility tend to focus on fewer but much larger deals. While Series A and B funding slowed across Africa in 2024, growth-stage investments remained strong, with mobility startups being a key beneficiary. Investors are drawn to established business models with clear profitability pathways, particularly those that incorporate financial services like vehicle financing and embedded payment systems. These sizable funding rounds reflect growing confidence in the sector’s ability to generate consistent revenue and scale effectively.

Revenue Potential

Logistics and mobility startups are uniquely positioned to benefit from Nigeria’s booming e-commerce market and advancements in digital financial services. By leveraging fintech-driven payment systems, these startups turn digital transactions into steady revenue streams. For example, OPay, a major player in logistics payments, reports monthly transaction volumes exceeding $12 billion.

The broader economic landscape also supports the sector’s growth. Nigeria’s ICT sector contributed 18.9% to the GDP in 2024, with predictions to hit 22% by 2025. Government initiatives are further fueling this momentum. In December 2024, the Nigeria Consumer Credit Corporation (CrediCorp) and the National Automotive Design and Development Council introduced a ₦20 billion consumer credit fund aimed at promoting locally assembled vehicle purchases. This move not only stimulates the automotive industry but also strengthens the mobility ecosystem.

With the synergy between e-commerce, fintech, and mobility, the sector is poised to become a key driver of economic growth in the coming years.

sbb-itb-dd089af

5. Cleantech

Investment Volume

Cleantech in Nigeria is still in its infancy. According to recent ecosystem reports, the energy and cleantech sector includes only 9 startups out of the 481 tech startups in the country – making up just about 1.8% to 1.9% of the tech ecosystem. By comparison, fintech dominates with 173 startups, representing a hefty 36% of the landscape.

When it comes to funding, the gap is even more striking. While fintech pulled in over $2 billion in investments in 2024, cleantech funding remains far smaller. The limited number of startups and the corresponding low investment levels highlight cleantech’s position as a niche, emerging sector within Nigeria’s broader tech ecosystem.

Share of Total Tech Funding

Cleantech currently captures only a sliver of Nigeria’s tech funding. Fintech alone accounted for an overwhelming 72% of total equity funding in 2024. With less than 2% representation in both startup numbers and funding, cleantech is still carving out its place. However, regulatory shifts, such as the Electricity Act, which decentralizes power governance, are beginning to create new opportunities for the sector. These changes suggest that cleantech could play a larger role in the future.

Revenue Potential

While sectors like fintech have already cemented their dominance, cleantech’s early-stage development presents a forward-looking investment opportunity. Its growth potential is tied to Nigeria’s evolving infrastructure. For instance, ICT contributed 18.9% to the nation’s GDP in 2024 and is expected to rise to 22% by 2025. Additionally, the telecom sector, fueled by 5G expansion, is projected to grow by 8–10%, which could indirectly support cleantech’s development.

Globally, cleantech aligns with sustainable technology trends, and Nigeria’s push for energy transition and decentralized power systems positions cleantech startups to meet local infrastructure needs while attracting international sustainability funding. However, the sector faces hurdles in building investor trust, as it lacks the scale and proven track record that fintech enjoys.

Nigeria to Boost Fintech Investment as World Bank–IMF Meetings Wrap Up

Advantages and Disadvantages

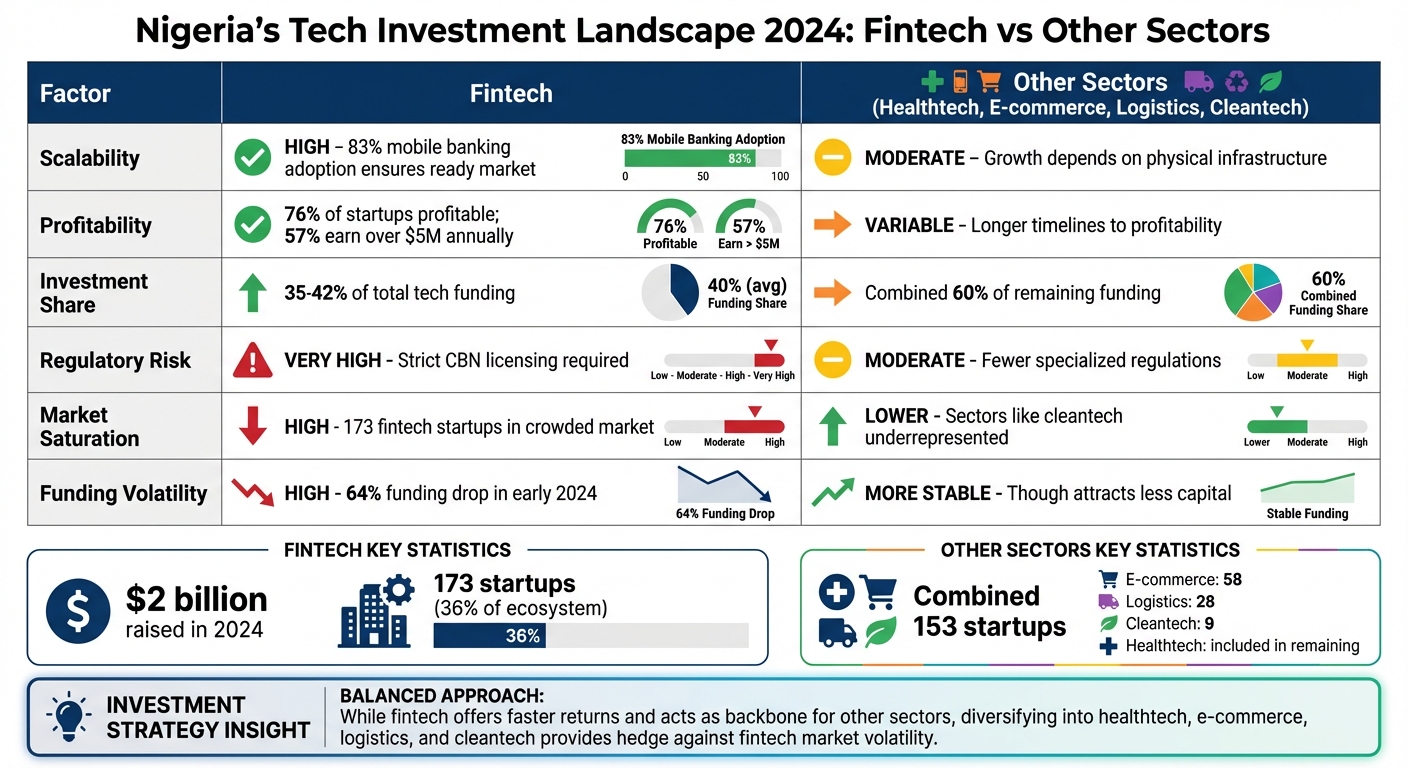

Nigeria Tech Investment by Sector 2024: Fintech vs Other Industries

Nigeria’s fintech sector offers a mix of promising opportunities and notable risks for investors.

A Look at Fintech’s Strengths

One of the biggest advantages of fintech in Nigeria is its scalability. With 83% mobile banking adoption, fintech companies can quickly expand their reach to a large, tech-savvy customer base. Financial services are a universal necessity, giving fintech a broad appeal and making it a cornerstone of the country’s tech ecosystem.

Regulatory and Market Challenges

However, the fintech space isn’t without its hurdles. It’s the most heavily regulated tech sector in Nigeria. Companies must secure strict licensing from the Central Bank of Nigeria (CBN) to handle public funds. This regulatory environment, while ensuring consumer protection, can be a significant barrier for new entrants.

Competition is another major challenge. With fintech startups making up 36% of Nigeria’s 481 startups, the market is crowded, and smaller players face the risk of being squeezed out. Adding to the uncertainty, fintech is particularly vulnerable to global economic shifts. For instance, equity funding for African fintech dropped by 64% to $221 million in the first half of 2024, reflecting the sector’s sensitivity to market contractions.

“Investors are demanding a lot more from founders and tech companies before committing to fund their ideas… reflecting a global response to high volatility and inflationary forces.” – Chinwe Michael

Exploring Other Sectors for Stability

While fintech has its clear advantages and risks, other sectors like e-commerce, logistics, healthtech, and cleantech offer a different kind of investment landscape. These industries face less regulatory scrutiny but often require longer paths to profitability due to higher operational costs and infrastructure needs.

Cleantech, for example, is an underfunded sector, representing less than 2% of startups. However, it holds potential for growth, especially as Nigeria continues its energy transition. These sectors, though not as immediately profitable as fintech, can provide a stabilizing effect during periods of fintech volatility.

Here’s a side-by-side comparison of fintech and other sectors to highlight their differences:

| Factor | Fintech | Other Sectors |

|---|---|---|

| Scalability | High; 83% mobile banking adoption ensures a ready market | Moderate; growth depends on physical infrastructure |

| Profitability | 76% of startups are profitable; 57% earn over $5M annually | Variable; longer timelines to profitability are common |

| Investment Share | 35–42% of total tech funding | Combined share of the remaining 60% |

| Regulatory Risk | Very high; strict CBN licensing required | Moderate; fewer specialized regulations apply |

| Market Saturation | High; 173 fintech startups in a crowded market | Lower; sectors like cleantech are underrepresented |

| Funding Volatility | High; funding contractions like the 64% drop in early 2024 | Generally more stable, though they attract less capital |

Balancing Investments

For investors, the key lies in striking a balance. While fintech often delivers faster returns and acts as a backbone for sectors like e-commerce and healthtech, diversifying into other industries can provide a hedge against the inherent volatility of the fintech market. Together, these sectors create a more resilient investment strategy.

Conclusion

Nigeria’s fintech sector is leading the charge in tech investment for 2024, reshaping the African tech landscape in the process. With an impressive 35% share of total tech funding, the sector has demonstrated remarkable resilience. Even more striking, 76% of fintech startups in Nigeria are already turning a profit, and the industry contributed 18.9% to the country’s GDP in 2024 – a figure projected to climb to 22% by 2025.

This dominance is rooted in solid fundamentals: mobile banking adoption stands at an impressive 83%, the population exceeds 200 million, and nearly half of adults remain unbanked, presenting significant growth opportunities.

“Nigeria’s fintech sector makes up about one third of Africa’s fintech market.” – Dahlia Khalifa, Regional Director at the International Finance Corporation

The fintech boom is also fueling growth in related sectors like healthtech, e-commerce, and cleantech. While these industries often face challenges in securing large-scale investments, they benefit from fintech’s infrastructure – such as payment gateways and digital wallets. With the rollout of 5G networks and increasing internet penetration, the number of online shoppers is expected to hit 122 million by 2025, further driving growth in these sectors.

Nigeria’s broader tech ecosystem is also set to thrive, with projections of over $3 billion in foreign investment by 2025. Fintech remains at the forefront, bolstered by an estimated $9 billion in unmet credit demand for small businesses.

“Nigeria’s fintech ecosystem, which attracted over $2 billion in investments in 2024, will continue to flourish in 2025, as digital financial services such as mobile banking, digital lending, and e-commerce expand.” – Office of the Special Adviser to the President on Economic Affairs

With its strong foundation and ripple effects across other industries, fintech is not only driving its own success but also positioning Nigeria as a leader in Africa’s digital economy. The country’s tech future looks brighter than ever.

FAQs

Why did Nigeria’s fintech sector attract a smaller share of tech investments in 2024 compared to previous years?

Nigeria’s fintech sector experienced a drop in its share of tech investments in 2024, driven by a mix of economic and industry-specific challenges. Rising inflation and economic struggles across Africa led to a tightening of venture capital funding. On a global scale, fintech funding shrank by about 20%, while investments in African fintech saw a sharper decline, falling 45% compared to the previous year.

Adding to the strain, the sector faced growing regulatory compliance demands and escalating cybersecurity expenses. These factors made the industry less appealing to some investors, further contributing to the reduced share of tech investments in Nigeria’s fintech space.

What challenges does Nigeria’s fintech sector face despite its rapid growth?

Nigeria’s fintech industry is booming, but it isn’t without its hurdles. One major obstacle is the country’s weak infrastructure. Frequent power outages and limited broadband access not only drive up operational costs but also slow down the adoption of digital payment systems, making it harder for businesses to scale.

Another significant challenge is cybersecurity. As financial services become increasingly digitized, cybercriminals have stepped up their game, leading to more advanced fraud schemes and hacking attempts. This forces fintech companies to invest heavily in security measures to protect their platforms and customers.

On top of that, economic pressures are squeezing both businesses and consumers. With inflation projected to hit 34.8% in 2024, consumer purchasing power is shrinking, which directly impacts revenue and profit margins for fintech companies.

Regulatory changes are also adding to the strain. New licensing requirements, open-banking rules, and foreign exchange policies have raised compliance costs, requiring companies to allocate more resources to meet these demands.

Lastly, the funding landscape has become more challenging. A tighter venture capital environment means startups now face tougher competition for a shrinking pool of investment opportunities, making it harder for new players to enter the market or for existing ones to expand.

These challenges highlight the complex environment in which Nigeria’s fintech sector operates, requiring resilience and adaptability from companies looking to thrive.

How is Nigeria’s fintech growth influencing other tech sectors like healthtech and e-commerce?

Nigeria’s fintech sector is not just pulling in massive investments – it’s also laying the groundwork for other industries like healthtech and e-commerce to thrive. In 2024, fintech claimed 35% of all tech investments in Nigeria, pushing forward innovations in digital payments, AI-powered tools, and regulatory systems. These advancements are proving invaluable for healthtech startups, helping them enhance diagnostics, streamline patient engagement, and optimize billing processes. Meanwhile, e-commerce platforms are benefiting from smoother payment systems and flexible credit options, including buy-now-pay-later services.

The impact of fintech is hard to overstate. With annual mobile-money transactions surpassing $1.68 trillion, fintech serves as the backbone for efficient financial services that other sectors can tap into. While it attracts a significant share of venture capital, programs like the World Bank’s $500 million small-business credit initiative are leveraging fintech solutions to empower healthtech providers and e-commerce businesses. By delivering essential tools, funding, and infrastructure, fintech is driving growth across Nigeria’s tech ecosystem in transformative ways.

Related Blog Posts

/* Shares”}};

/* ]]> */